The Federal Reserve is expected to cut rates this September, and many people are asking the same question: how will this affect mortgage rates? Let’s walk through what you need to know.

Looking Back at 2024

Last year shows us how mortgage rates often behave:

- September 18, 2024: The Fed cut short-term rates by 0.50%

- November 6, 2024: Another 0.25% cut

- December 18, 2024: A further 0.25% cut

You might expect mortgage rates to fall right along with these cuts. But that’s not what happened. Mortgage rates had already dropped by about 0.625% in August, before the Fed made the first move in September. The market anticipated the cuts ahead of time.

Why Mortgage Rates Don’t Wait for the Fed

Mortgage rates are influenced by more than just the Fed’s decisions:

- Rates often move before an announcement. Investors try to stay ahead, so expectations are priced in early.

- Other factors matter too. Inflation, jobs data, and global demand for U.S. bonds all affect long-term rates like the 10-year Treasury.

- Stronger economic reports can push rates higher. Even if the Fed is lowering rates, hot inflation or strong job growth can cause mortgage rates to rise.

In short, mortgage rates are connected to Fed policy but not controlled by it.

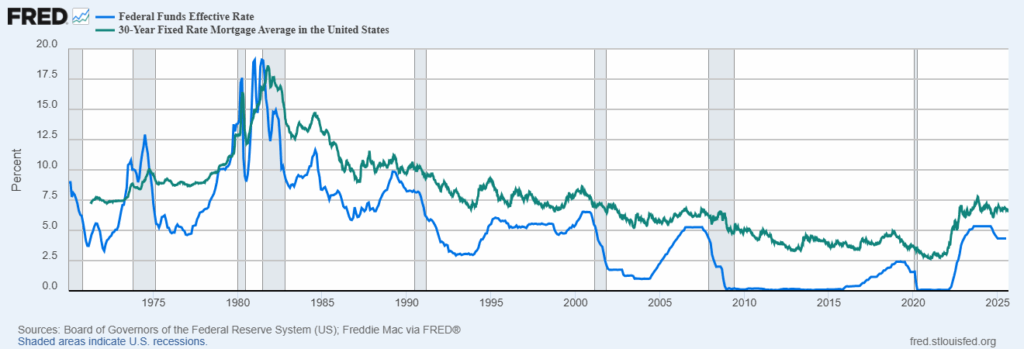

A long-term chart shows a correlation between the Fed Funds Rate and mortgage rates, but it’s not a lockstep relationship. Mortgage rates are guided by broader economic forces.

What’s Happening Now

Mortgage rates have dipped to their lowest point this year. Why? Because the market already expects the Fed’s September cut and has reacted to softer inflation data.

Here’s what this means for you:

- Home buyers: You can lock in lower borrowing costs than we’ve seen in months.

- Homeowners: Many will refinance twice in the next few years, once now for immediate savings, and again later if rates fall further as the economy steadies.Gives you more options if you want to sell or refinance.

The Bottom Line

Do not wait for the official Fed announcement. By the time it hits the news, the benefit is usually already built into mortgage rates.

If you are thinking about buying or refinancing, now is a smart time to review your options. I can help you with timing, strategy, and choosing the right loan for your situation.

FAQs About the September 2025 Rate Cut and Mortgage Rates

Will the Fed rate cut lower mortgage rates immediately?

Not always. Mortgage rates often move before the Fed announces a cut. Markets anticipate changes, so rates may already reflect the expected move.

Why don’t mortgage rates always follow the Fed?

The Fed controls short-term rates, but mortgage rates are tied to long-term trends like inflation, jobs data, and global demand for U.S. bonds.

Are mortgage rates lower right now?

Yes. Mortgage rates recently dipped to their lowest levels of the year because investors expect a September Fed cut and softer inflation.

Should I refinance now or wait?

Many homeowners may benefit from refinancing now and potentially refinancing again later if long-term rates fall further. Acting early helps lock in current savings.

Is this a good time to buy a home?

For many buyers, yes. Lower mortgage rates make borrowing more affordable, which can increase purchasing power.